ZAKAT ON BUSINESS

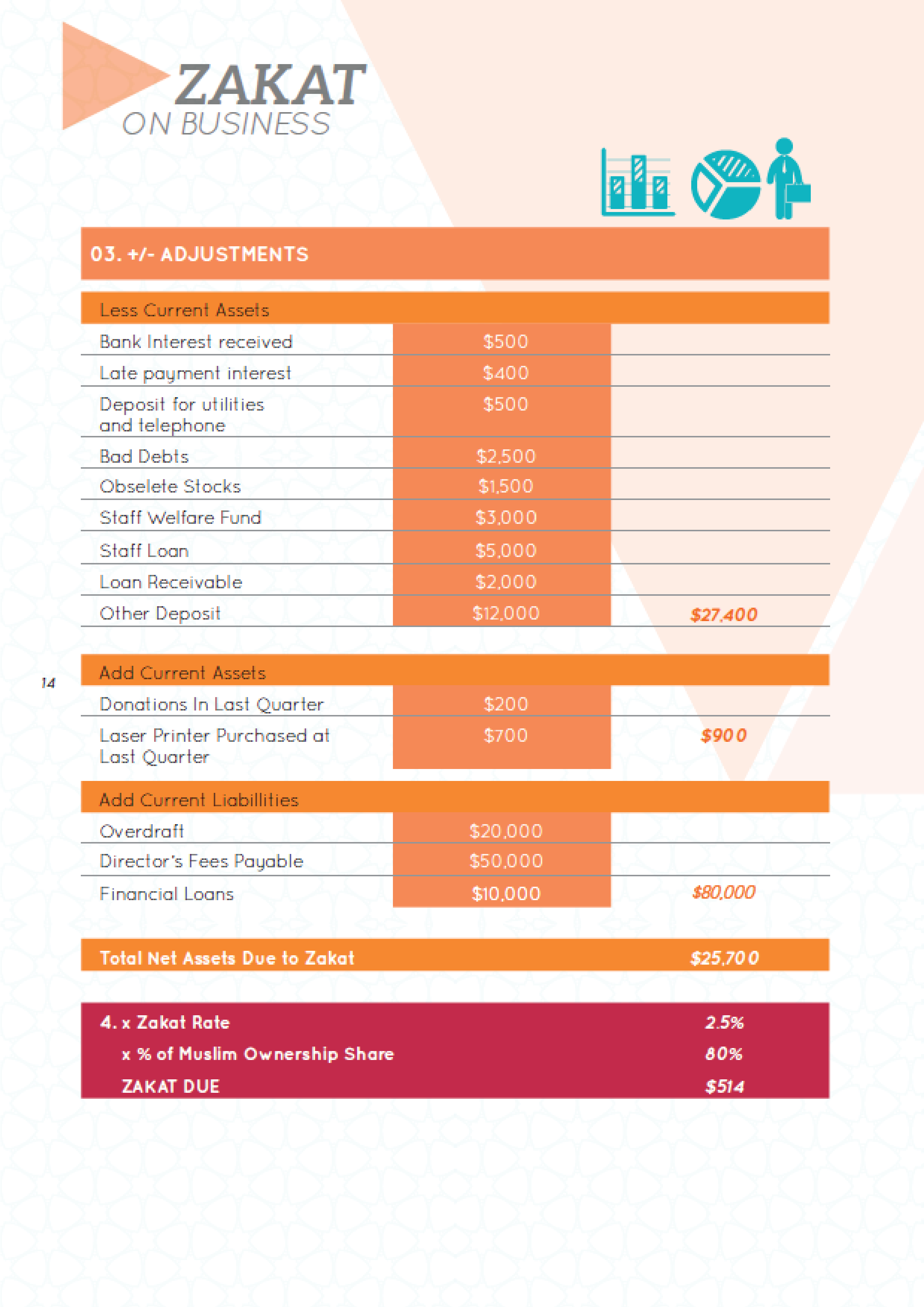

The computation of Zakat on Business is based on the *Working Capital Model (Shariah) that includes current assets, excludes current liabilities, and considers adjustments at year end.

The Accounting and Auditing Organisation for Islamic Financial Instituitions (AAOIFI) FAS 9 sets out accounting rules related to Zakat on Business.

The intention or purpose for business must be made when an asset becomes part of the business that is conducted in order to gain profit.

Other Types of Zakat Harta

Zakat on Savings

Zakat on Gold (Intended for Usage)

Zakat on Gold (Not Intended for Usage)

Zakat on Insurance

Zakat on Shares

Zakat on Business

Zakat Fitrah

GUIDE ON ZAKAT ON BUSINESS

Contact Us Now ! 6359 1199

For enquiries and appointments

Contact Us Now ! +65 6359 1199

For enquiries and appointments